Managing personal finances can feel overwhelming when you’re just starting out. Between paying bills, saving money, and planning for the future, it’s easy to make mistakes that can affect your financial well-being. The good news is that building strong financial habits doesn’t require advanced knowledge or a high income. Small, consistent actions can create a solid foundation for long-term financial success.

Whether you’re entering the workforce, starting a family, or simply looking to improve your money management skills, developing healthy financial habits is one of the best investments you can make in yourself.

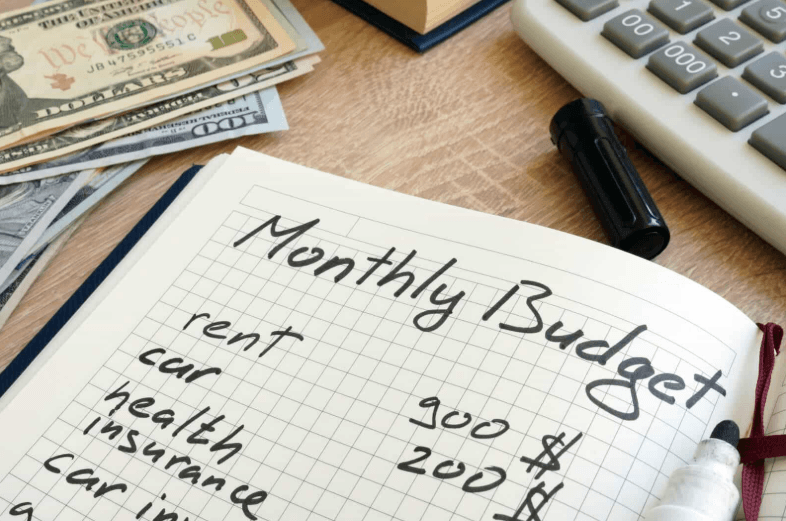

1. Create and Follow a Budget

A budget is the cornerstone of personal finance. It helps you understand where your money is going and ensures that your spending aligns with your priorities.

Start by listing your monthly income and all expenses, including:

- Rent or mortgage payments

- Utilities

- Groceries

- Transportation

- Insurance

- Entertainment

- Savings contributions

Many people find success with the 50/30/20 rule:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

Tracking your expenses regularly helps identify areas where you may be overspending and allows you to make adjustments before financial problems arise.

2. Track Every Expense

One of the most common reasons people struggle financially is that they underestimate their spending. Small purchases can quickly add up over time.

Using budgeting apps or maintaining a simple spreadsheet can help you monitor your daily expenses. When you know exactly where your money goes, you’re more likely to make informed financial decisions.

Just as people use digital platforms such as the parimatch app to conveniently manage their online activities, personal finance apps can help individuals monitor spending, savings, and financial goals in one place.

3. Build an Emergency Fund

Unexpected expenses are a part of life. Medical emergencies, car repairs, job loss, or home maintenance costs can quickly strain your finances if you’re not prepared.

An emergency fund acts as a financial safety net.

Financial experts generally recommend saving:

- At least three to six months of living expenses

- More if your income is irregular or self-employed

Start small if necessary. Even saving a modest amount each month can gradually build a meaningful reserve.

4. Avoid Unnecessary Debt

Debt can be useful when managed responsibly, but excessive borrowing can limit your financial freedom.

Before taking on debt, ask yourself:

- Is this purchase truly necessary?

- Can I afford the monthly payments?

- Will the debt improve my financial situation in the future?

High-interest debt, particularly from credit cards, should be minimized whenever possible. Paying balances in full each month helps avoid costly interest charges and protects your credit score.

5. Save Before You Spend

Many people save whatever money remains at the end of the month. Unfortunately, there is often little left to save.

A better strategy is to “pay yourself first.”

When you receive your income:

- Transfer a portion directly into savings.

- Allocate funds toward investments.

- Then manage your remaining expenses.

Automating savings transfers makes this process easier and helps build consistency.

6. Set Clear Financial Goals

Goals provide direction and motivation. Without them, it’s easy to lose focus and spend money impulsively.

Examples of financial goals include:

- Building an emergency fund

- Buying a home

- Starting a business

- Paying off debt

- Funding higher education

- Saving for retirement

Break larger goals into smaller milestones. Achieving these smaller targets creates momentum and keeps you motivated.

7. Learn Basic Investing Principles

Saving money alone may not be enough to achieve long-term financial growth. Inflation gradually reduces purchasing power, making investing an important component of wealth building.

Beginners should focus on understanding:

- Stocks

- Bonds

- Mutual funds

- Index funds

- Retirement accounts

You don’t need to become a financial expert overnight. Consistent learning and gradual investing can significantly improve your financial future.

8. Review Your Finances Regularly

Financial planning is not a one-time activity. Your circumstances, income, expenses, and goals will change over time.

Schedule a monthly financial review to:

- Check spending patterns

- Update your budget

- Monitor savings progress

- Evaluate investments

- Adjust financial goals

Regular reviews help you stay accountable and make timely corrections when necessary.

9. Improve Financial Literacy

Financial education is one of the most valuable investments you can make.

Read books, follow reputable financial websites, listen to podcasts, and learn from trusted financial professionals. The more knowledge you gain, the more confident you’ll become in making financial decisions.

Important topics to understand include:

- Compound interest

- Credit scores

- Taxes

- Insurance

- Retirement planning

- Investment diversification

Even dedicating a few minutes each week to learning can lead to substantial long-term benefits.

10. Practice Delayed Gratification

One of the strongest financial habits is learning to delay non-essential purchases.

Before making a significant purchase, consider waiting 24 to 48 hours. This simple habit reduces impulse spending and allows you to evaluate whether the purchase truly aligns with your priorities.

Over time, this mindset can lead to greater savings, lower debt, and more thoughtful financial decisions.

Conclusion

Personal finance is less about earning a huge income and more about developing consistent habits. Creating a budget, tracking expenses, building an emergency fund, saving regularly, and continuing to learn about money management are all powerful steps toward financial security.

The earlier you adopt these habits, the more time you give yourself to benefit from compounding growth and disciplined financial decision-making. By focusing on small improvements and staying consistent, even beginners can build a strong financial future and achieve their long-term goals with confidence.